-

Zombie, Over-Levered, or Shocked-but-Sound? Pandemic-Induced Bankruptcies and Related Valuation Questions

What valuation challenges may lie ahead for companies led into bankruptcy from pressures of the novel coronavirus pandemic?

Shocks from the coronavirus pandemic have placed and will continue to place an enormous strain on the global economy and US businesses. We have already seen a wave of bankruptcies beginning across many sectors, including hospital operators (e.g., Quorum Health Corp.), restaurants (e.g., FoodFirst Global Restaurants), and major retailers (e.g., J.Crew). While the path to economic recovery remains uncertain, it seems clear that, for some companies in particularly hard-hit industries, the path is likely to lead through US bankruptcy courts.

Even in less extraordinary times, company valuation is often a major point of contention amongst various shareholders and creditors in a Chapter 11 proceeding. These valuation disagreements will escalate as bankruptcy courts and valuation experts are challenged to restructure claims amidst the current level of economic uncertainty.

This uncertainty – arising from the widespread and potentially long-term economic impact of the pandemic – poses challenges for estimating the value of a company. These challenges can be overcome, we believe, by exploring the effects of the pandemic on the basic building blocks of valuation: estimated free cash flows and the cost of capital.

On the following pages, we first examine questions that the pandemic raises for these two building blocks, recognizing that each company will present special business-specific issues that must also be factored into a valuation inquiry.

We then discuss three types of companies that may be more likely to enter bankruptcy courts, categorized based on their pre-pandemic financial condition: “shocked-but-sound,” “over-levered,” and “zombie” companies. While any one company may not fit neatly, or even exclusively, into a particular category, each category raises special valuation challenges that will need to be considered.

Cash Flows Cost of Capital Fundamentals

- Projected cash flows depend on the expected trajectory of revenues, operational costs, working capital, and investments in fixed assets.

- Although projections are often prepared by corporate managers for use in Chapter 11 proceedings, it is critically important to explore cash flow trajectories under alternative assumptions about the future, especially as uncertainty about the future increases.

- In bankruptcies, opposing experts are likely to challenge each other’s estimates of the weighted average cost of capital (WACC), which provides the discount rate applied to financial projections.

- Calculating a business’s WACC involves well-established theoretical foundations, including the cost of equity, cost of debt, and capital structure weights.

- The three primary inputs for estimating the cost of equity on a going-forward basis – which are often flashpoints for disagreement, but are particularly challenging to estimate in the current environment – are the predicted risk-free rate, the equity risk premium, and the company’s beta.

Key Questions

- How do cash flow trajectories vary with the shape of the anticipated economic recovery – swoosh-shaped, V-shaped, U-shaped, W-shaped, or an even worse shape?

- To what extent does the business rely on labor inputs? What new operational costs will be borne in order to maintain appropriate distancing in the workplace?

- How will social distancing affect the delivery of goods and services to customers? Will the shift to online shopping and delivery become permanent for retail, restaurants, and other sectors? Will telemedicine continue to grow?

- How will cash flow projections be impacted by supply chain disruptions, particularly for materials sourced overseas?

- To what extent has the company delayed long-term investments because of quarantines?

- The risk-free rate is usually taken from long-term Treasury bonds. How should the risk-free rate be measured if investors flock to Treasuries during the economic crisis, depressing yields?

- The equity risk premium is the spread between the return on a well-diversified portfolio such as the S&P 500 and the risk-free rate. If historical averages become less relevant to future conditions, how should the equity risk premium be measured?

- Beta is a measure of the sensitivity of a company’s equity returns to overall market risk. Will that sensitivity change on a going-forward basis such that historical patterns are an inappropriate proxy?

“Shocked-but-Sound”

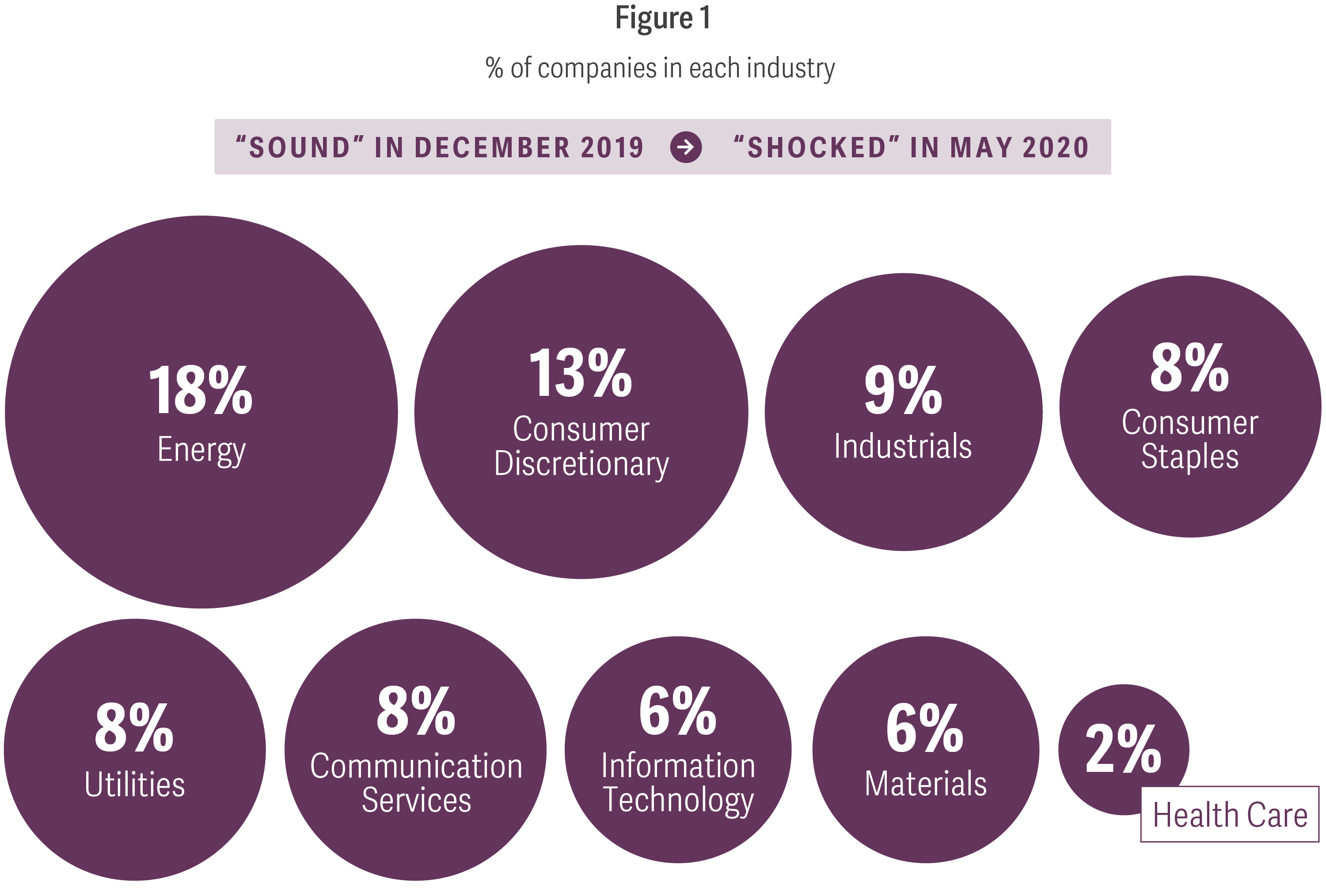

“Shocked-but-sound” businesses had promising futures before the pandemic, but may now face a short-term liquidity crisis. Although there is no “bright line” test for determining whether a business is facing a short-term liquidity crisis, a high market leverage ratio – that is, the ratio of net debt (debt minus cash) to market capitalization – can cast doubt on a company’s ability to meet its short-term obligations. To identify “shocked-but-sound” businesses, we calculated market leverage ratios for all nonfinancial companies in the Russell 3000 as of December 2019. Next, we categorized businesses into nine industries and identified, by industry, the leverage ratio that separated the top 10% of companies (as measured by market leverage) from the remaining 90%. Finally, we identified companies that were below this threshold in December 2019, but above it as of May 2020. (See Figure 1.)

These companies are “shocked-but-sound” because they suddenly jumped from a relatively low leverage ratio to a high leverage ratio during the pandemic. The jump is due entirely to investor devaluation of the companies’ equity because our measurement of net debt does not change during this period.

Key Valuation Considerations: A “shocked-but-sound” company is healthy, but experiencing a short-term liquidity crisis. Whether a company’s long-term financial position truly places it into this category depends on projected future cash flows. If equityholders believe that their company falls into this category in the long term, we can anticipate a contentious valuation battle in bankruptcy court, with equityholders demanding a recovery and creditors questioning whether the future cash flows will be sufficient to warrant such a recovery. To avoid these fights, a company may consider issuing options such as warrants to equityholders, which could allow them to buy back shares at a price that ensures full payment to creditors.

Click on the graphic below to open up an interactive version

“Over-Levered”

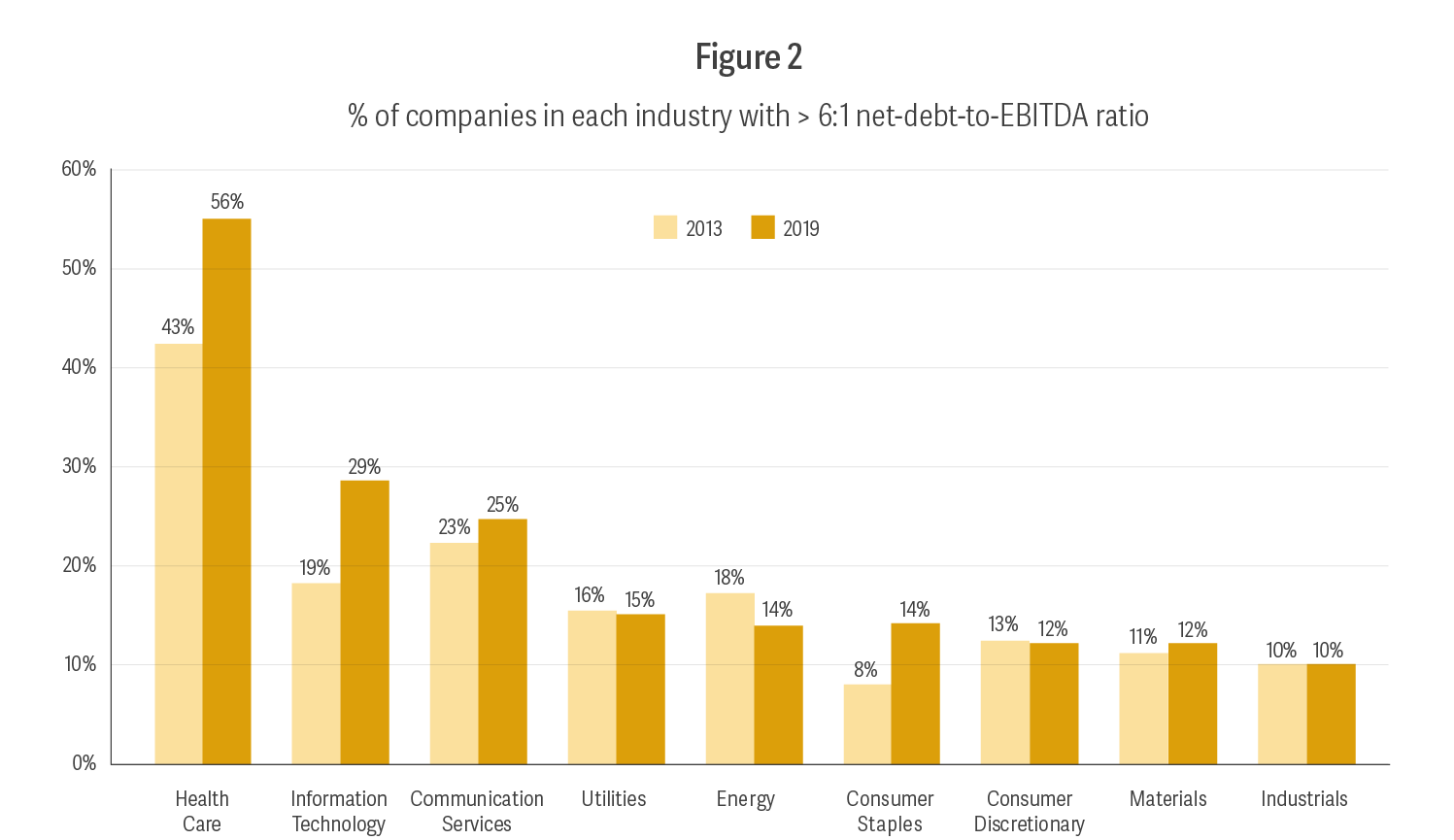

Many companies entered the crisis with pre-existing weaknesses in their balance sheets. A decade of low interest rates induced a substantial number of businesses to increase their debt levels and thus their leverage ratios. With liabilities now exceeding assets, these companies may be facing a solvency crisis that pushes them into bankruptcy court. We refer to these companies as “over-levered.”

Figure 2, using the same industry groupings as in the “shocked-but-sound” analysis, shows the percentage of companies in each industry that had a net-debt-to-EBITDA ratio greater than 6:1, as of 2013 and as of 2019. A 6:1 ratio is often considered a red flag, and is used as a threshold for the Federal Reserve’s Main Street Expanded Loan Facility Program.

Key Valuation Considerations: In contrast to a “shocked-but-sound” company, where we may see shareholders arguing that it is solvent going forward, the flashpoint in cases involving “over-levered” companies is likely to be the point in the capital structure where creditors will need to take haircuts. Where in the valuation waterfall will the payouts end? At secured debt? Or are junior creditors entitled to a recovery? With the uncertainty surrounding future cash flows in the current economic environment, companies may consider ways to forestall protracted battles over these questions. One strategy is to issue warrants to junior creditors, allowing them an option to buy into the capital structure at a future date.

Click on the graphic below to open up an interactive version

“Zombies”

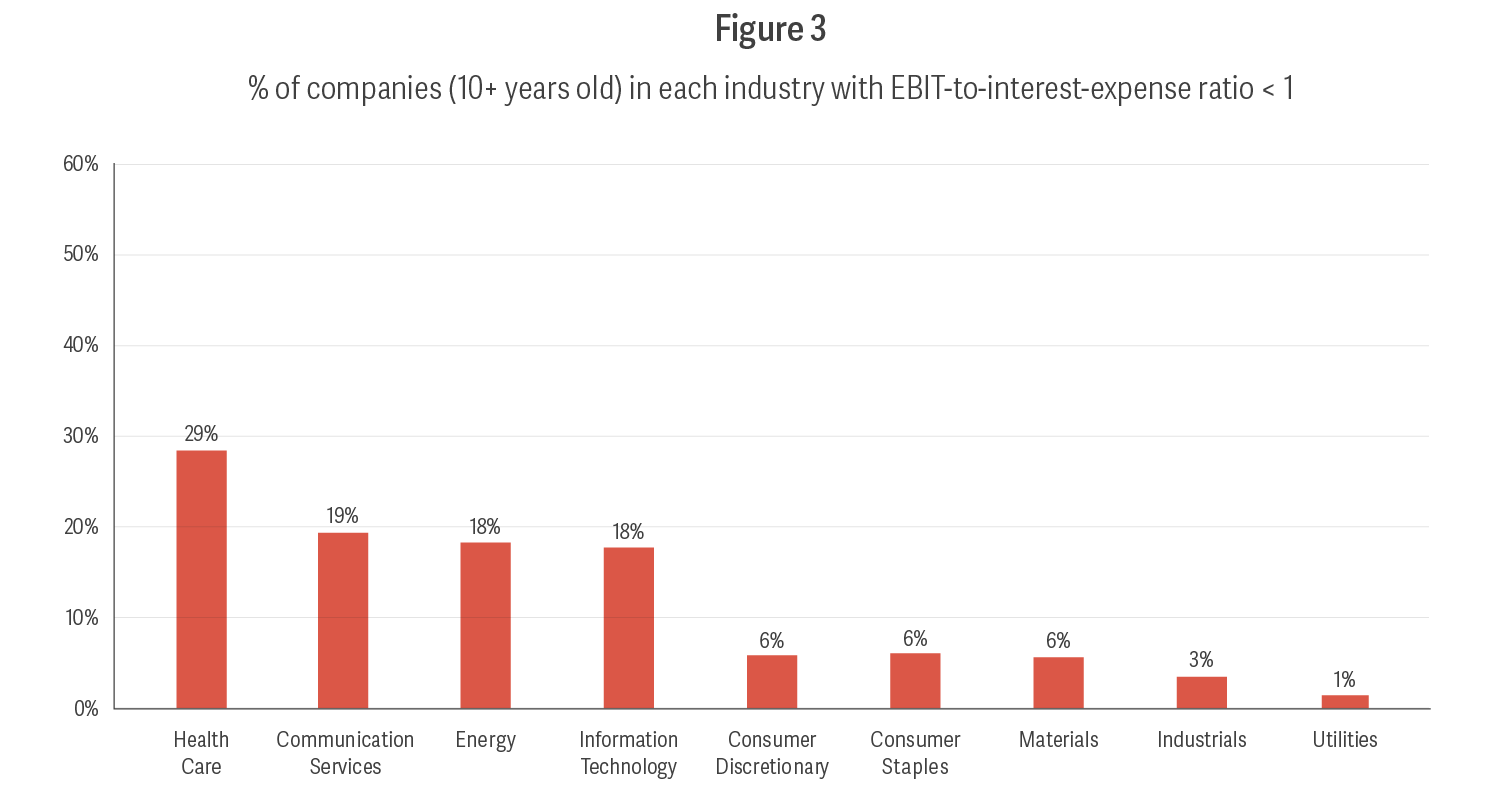

The weakest companies are likely to face the most severe challenges posed by the economic fallout from the pandemic. We call these companies “zombies,” using the definition adopted by the Bank of International Settlements (BIS) – businesses that are at least 10 years old and have a ratio of EBIT to interest expense that is below one for three consecutive years. Figure 3 shows the percentage of “zombies” in each industry, based on data from 2017 through 2019.

Like “over-levered” companies, these corporate “zombies” were already struggling before the pandemic, with cash flows insufficient to service their debt obligations. They have managed to remain solvent to date primarily through their lenders’ forbearance. For many of these businesses, the increased financial distress resulting from the pandemic may be the final straw that pushes them into bankruptcy courts.

Key Valuation Considerations: “Zombies” have struggled for years to generate cash flows sufficient to pay interest expense. For many of these companies, years of limited cash flows may have resulted in underinvestment in critical areas, such as research and development and infrastructure. When zombies enter bankruptcy, then, it may be challenging to resuscitate their businesses. If so, the companies may be presented with the prospect of being sold off (in pieces or as a whole). Even those that reorganize may emerge from bankruptcy with a smaller scale of operations. Unlike “shocked-but-sound” and “over-levered” companies, for whom the flashpoint in bankruptcy will often be the point in the capital structure where creditors begin to take haircuts, zombies will present questions related to the viability of existing operations and the value of assets (which may be depressed temporarily during the pandemic).

Click on the graphic below to open up an interactive version

Conclusion

In the months ahead, the pandemic’s economic fallout is likely to magnify the wave of Chapter 11 filings already observed across various industries. Some Chapter 11 filers will fit the profiles of prototypical bankruptcy cases: Companies with viable businesses but unsustainable leverage, at least in the current economic environment. These “over-levered” filers will be joined in bankruptcy court by a number of “zombies” – companies that have suffered years of distress and may require more than just balance-sheet restructuring.

Less common bankruptcy filers are “shocked-but-sound” companies that are suffering a temporary liquidity crisis. These too, however, may account for a sizable number of cases going forward, at least in the near term.

After their arrival in bankruptcy court, all of these companies will face valuation challenges specific to their businesses, and these challenges will be made more complex by the great uncertainty in the current economic environment. These challenges are manageable, however, as long as experts pinpoint the effects of the current pandemic on the building blocks of valuation – modeling free cash flows and estimating the discount rate – that have strong foundations in theory and evidence. ■

-

Forum: 2020

From Forum 2020.